14

Dependents working part-time in Japan: Key income thresholds to know for 2025–2026

Japan's 'income wall' (年収の壁) during the 2025–2026 reform period — one of the biggest changes to tax and social security policy in three decades.

Scope note: This article compiles and analyses regulations on income tax, residency tax, and social insurance for dependents (扶養) in Japan during the 2025–2026 reform period. The examples at the end are illustrative, and specific calculations are estimated for reference.

1. Background: Why is the system changing?

For the past 30 years, the 1.03 million yen income tax exemption threshold has remained virtually unchanged, while Japan's minimum wage has steadily risen. This has created a paradox: more people are becoming "trapped" at the 1.03 million yen threshold for fear that exceeding it will result in losing tax and insurance benefits, leading to the phenomenon of "work restraint" (働き控え), which wastes human resources.

The 2025–2026 period marks the most extensive reform in three decades, proceeding along two parallel tracks:

- Expanding tax thresholds (to free up labour)

- Tightening social insurance exemption conditions (to broaden social security coverage)

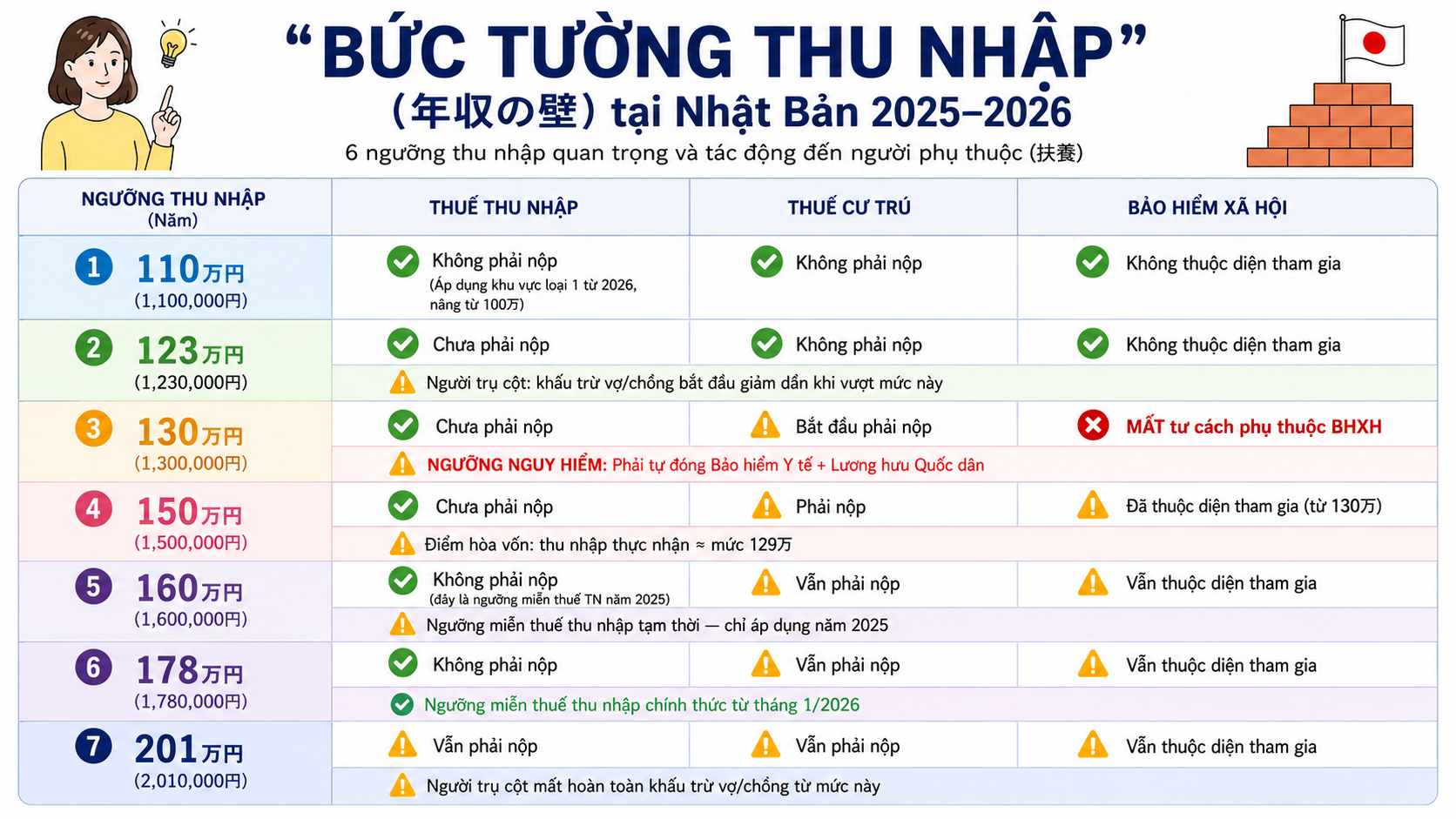

2. Map of income thresholds for 2025–2026

2.1. The 1.1 million yen threshold — Residency tax (市民税・県民税)

From fiscal year 2026 (based on 2025 income), the residency tax exemption threshold will be raised from 1 million yen to 1.1 million yen in Category 1 areas (Tokyo's 23 wards, Osaka, Nagoya, and equivalent major cities).

However, this threshold depends on the regional classification (級地区分) of the place of residence:

Note: Residency tax consists of two parts: an income-based portion (所得割) and a flat-rate portion (均等割). Being exempt from this threshold means exemption from both. Additionally, from 2024, Japan has added a "Forest Environment Tax" of 1,000 yen per year — unless the individual is fully exempt from tax.

2.2. The 1.23 million yen threshold — Spousal deduction (配偶者控除)

From 2025, for the main earner (with an income below 9 million yen) to receive the maximum deduction of 380,000 yen from income tax, the dependent's income must be below 1.23 million yen (previously 1.03 million yen).

If the income is not from wages, the limit is income after expenses of less than 580,000 yen.

Special spousal deduction (配偶者特別控除) when exceeding 1.23 million yen:

Main earner income limit: If wage income exceeds 11.95 million yen (equivalent to taxable income of 10 million yen), no spousal deduction of any kind is applicable.

2.3. The 1.3 million yen threshold — The social insurance wall (most important)

This is the threshold that has not changed and carries the greatest potential financial risk. When income exceeds 1.3 million yen, the dependent loses eligibility for insurance under their spouse and is required to pay National Health Insurance and National Pension contributions themselves.

The "income reversal" phenomenon (逆転現象)

Based on simulations from Japanese financial institutions cited in reference materials:

→ If you have already exceeded 1.3 million yen, aim for at least 1.5 million yen to offset the additional insurance costs.

2-year exception

If income exceeds 1.3 million yen due to "temporary overtime" or "unexpected extra work" (not a base salary increase or a permanent contract change), the employer can issue a certificate allowing the worker to maintain dependent status for up to two consecutive years.

2.4. The 1.6 Million Yen Threshold – Temporary Income Tax (2025)

In 2025, based on the "Act Partially Amending the Income Tax Act," the income tax exemption threshold will be raised to 1.6 million yen through:

- Employment income deduction: increased from 550,000 yen to 650,000 yen (+100,000 yen)

- Special basic deduction: increased from 480,000 yen to a maximum of 950,000 yen (+470,000 yen) – applicable only to the income group below 2 million yen

This 950,000 yen basic deduction is a temporary measure, expected to be reviewed after 2027.

2.5. The 1.78 Million Yen Threshold – Official Income Tax from 2026

From January 2026, following an agreement between the Liberal Democratic Party (LDP) and the Democratic Party for the People (DPP), the income tax exemption threshold will be raised to 1.78 million yen.

The figure of 1.78 million yen is calculated based on the minimum wage growth factor over approximately 30 years (roughly 1.73 times the 1.03 million yen threshold). A key new feature is the introduction of a "Slide system" – deduction levels will be automatically adjusted according to the consumer price index, preventing "bracket creep" caused by inflation.

2.6. The 2.01 Million Yen Threshold – Complete Loss of Spousal Deduction

When a dependent's income reaches 2.016 million yen or more, the main breadwinner is no longer eligible for any deduction. This threshold remains unchanged during the 2025–2026 period.

3. Major Changes to Social Insurance at the Workplace

3.1. Abolition of the 88,000 Yen Monthly Salary Standard (from October 2026)

Currently, the conditions for mandatory enrolment in company social insurance include three criteria: working over 20 hours per week, a monthly salary over 88,000 yen, and working at a company with over 50 employees.

From October 2026, the "monthly salary of 88,000 yen" standard will be completely abolished. The reason: continuous minimum wage increases mean that most people working over 20 hours per week already naturally exceed this level. The remaining condition will simply be:

Working over 20 hours per week at an eligible company → mandatory social insurance enrolment, regardless of income.

3.2. Roadmap for Expanding Company Size Thresholds

From October 2029, the regulations will also extend to individual business operators in all industries (including food services and accommodation – previously only applicable to 17 legally designated industries).

3.3. Support for Businesses (Career Up Grant)

The Ministry of Health, Labour and Welfare is implementing subsidies for businesses:

- Up to 750,000 yen per person if the business increases working hours or raises wages so that employees can join social insurance without a reduction in their actual income.

- For the first three years of application for small companies, business owners can choose to increase the company's share of insurance premium contributions (instead of the 50/50 split), with the government fully covering the difference.

4. Practical Example: Foreign National on a Dependent Visa (配偶者ビザ), 28-Hour Weekly Limit

A foreign national holding a dependent visa (spouse) is granted permission by Japan's Immigration Services Agency to engage in activities outside their status of residence (資格外活動許可) with a maximum limit of 28 hours per week. This is a strict legal constraint, unrelated to tax or social insurance thresholds.

Assumed conditions for the example: Working at a company with over 51 employees (currently meeting mandatory social insurance conditions). The net income figures are illustrative estimates based on simulations cited in reference materials – not official legal figures.

Case A: Keeping Income Below 1.1 Million Yen/Year

- Income tax: Exempt

- Residence tax: Exempt (in Category 1 areas from 2026)

- Dependent social insurance status: Maintained

- Spousal deduction for the main breadwinner: Maximum 380,000 yen

- No additional obligations arise. → A strategy of absolute safety. Suitable if prioritising procedural simplicity.

Case B: Income from 1.1 million to 1.29 million yen/year (working 28 hours/week)

This is the range where many people working 28 hours a week on an average salary may fall.

- Income tax: Exempt (under 1.6 million yen in 2025, under 1.78 million yen from 2026)

- Residence tax: A small amount incurred if exceeding 1.1 million yen (Category 1) or 1.03 million yen (Category 3)

- Dependent status for social insurance: Maintained (under 1.3 million yen)

- Spousal deduction: Full 380,000 yen if under 1.23 million yen; shifts to a special deduction if between 1.23 million and 1.29 million yen (still eligible)

⚠️ Important warning: 28 hours/week exceeds the 20 hours/week threshold. From October 2026, at companies with over 51 employees, working 28 hours/week will trigger mandatory enrolment in the company's social insurance scheme — regardless of income level. You should discuss this with your human resources department before this date.

→ Good from a tax perspective, but preparation is needed for the social insurance change from October 2026.

Case C: Income exceeding 1.3 million yen/year — The danger zone

- Loss of dependent status for social insurance → must independently enrol in National Health Insurance + National Pension

- Or: if the company meets the criteria and you work 28 hours/week → enrol in the company's social insurance (company pays 50%)

- Actual take-home pay at 1.31 million yen could be lower than when earning less (see table in section 2.3)

Ways out:

- Two-year exception: If exceeding 1.3 million yen is due to temporary overtime (not a permanent salary increase) → ask the company to issue a certificate to maintain dependent status for a maximum of two additional years.

- Break through to 1.5 million yen+: If the exception cannot be used, aim for at least 1.5 million yen to break even with the incurred insurance costs.

→ Avoid the 1.3 million to 1.49 million yen range if no specific solution is in place.

Case D: Income from 1.5 million yen or more — Breaking through

- Income tax: Exempt (under 1.6 million yen in 2025; under 1.78 million yen from 2026)

- Residence tax: Payable

- Social insurance: Self-enrolment (or via the company if working 28 hours/week from October 2026)

- Actual take-home pay: Begins to exceed the 1.29 million yen level from around 1.5 million yen

- Long-term benefits: Accumulates welfare pension (厚生年金), eligibility for disability and maternity benefits

→ The direction the government encourages. Suitable if aiming to build a long-term social security foundation.

Quick Summary

A specific note for those working 20 hours/week or more at companies with over 51 employees (excluding international students): From October 2026, the 88,000 yen/month salary standard is abolished, meaning that working 20 hours/week or more will mandate participation in the workplace social insurance scheme regardless of income. For those working the maximum of 28 hours/week, they are already effectively required to enrol due to rising minimum wages. Therefore, if you wish to maintain your dependent insurance status, you should proactively discuss with your human resources department to adjust your working hours (to below 20 hours/week) before this date.

Comments

No comments yet. Be the first!

You need to sign in to comment.